Funding Disruption: Why Startups Shouldn't Wait to Plan their Real Estate Needs

SILICON VALLEY BANK COLLAPSE

As We Dust Off from the Fallout, What Have We Learned, and How Do We Move Forward?

The fallout of Silicon Valley Bank (SVB) and the impacts it has had on the financial sector will disrupt the life science industry and scientific real estate sector. SVB’s focus on the tech ecosystem and their aggregation model allowed the firm to build a network effect that tapped into local talent and gave companies access to venture capitalists, private equity, and other sources of funding. Their specialization in the world of startups and high growth companies focused on new technologies and disruptive innovations that was a differentiator for the industry. More specifically, prior to their collapse, SVB’s loans increased to $74.3B1 as of December 31, 2022, driven primarily by “global fund banking, technology, and [most relevant] life science/healthcare.”2

So, what really happened? In short, unrealized losses. The bank’s business model lacked diversification given their focus on providing uncollateralized loans to the startup economy and was generating a ton of cash. In order to grow their balance sheet, they purchased fixed HTM3 securities which yielded competitive returns at the time. Enter a rise in US treasuries and the bond’s fair value started falling below levels SVB had purchased them, nor could they sell them, which was their primary means of raising liquidity to pay their depositors. Falling bond yields led many investors and depositors to become uncertain of the bank’s liquidity given the “truth” behind their unrealized losses - then came the bank run.

SVB underscored their liquidity risks such that “…an inability to maintain or raise funds through these sources could have a substantial negative effect, individually or collectively, on SVB Financial and the Bank’s liquidity [and] a downturn in asset markets such that the collateral we hold cannot be realized or is liquidated at prices not sufficient to recover the full amount of our secured obligations.”4

The ripple effect on the regional banking system over the past several weeks is well documented as are uncertainties for additional interest rate hikes. Clients are attempting to shore up their accounts and creditors are tightening their belts as we enter a more turbulent market environment. The sudden failure left numerous companies scrambling to secure alternative funding, potentially stalling progress in research and development, and delaying the commercialization of groundbreaking therapies because science never stops. The sudden withdrawal of capital meant firms had to shift to short-term operational stability rather than focusing on breakthrough product innovation and scalability.

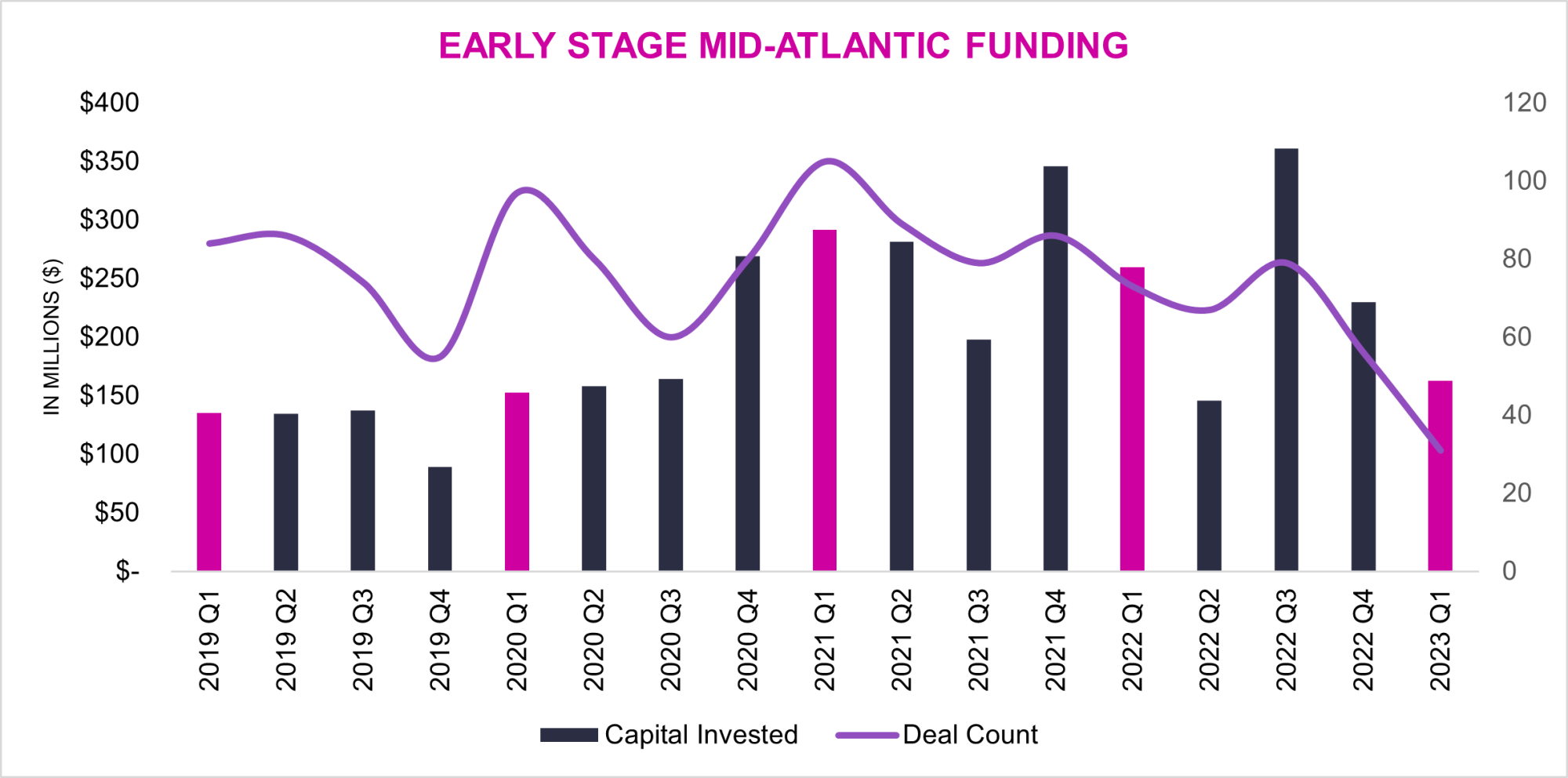

Source: Pitchbook, Scheer Partners. Biopharma & Lifesciences. Mid-Atlantic by State

The scientific real estate market, which has been thriving due to the continued expansion of the life science sector, faces uncertainty as investors and developers assess the demand for specialized lab and research facilities. While the COVID-19 pandemic certainly fueled record investments into the sector, many companies have been formed around single technologies – which are becoming a “thing of the past.” The full extent of the impact remains to be seen. As recent events continue to unfold, there are consequences for innovation, investment, and growth in industry, and most importantly, the associated real estate market implications, could be significant in the Mid-Atlantic5. For the industry to transcend to its next phase, the venture community must take on a “big pharma mentality” to pool technologies and form larger parent companies that have multiple assets in their immediate pipeline.

After several years of record setting quarters, the total number of deals in the Mid-Atlantic dropped 58% in Q1 236 trending toward pre-pandemic levels more closely resembling 2019 than the past two years (92 in Q1 21 & 93 in Q1 22) for early-stage companies predominantly in biotechnologies, drug discovery, and pharmaceuticals. While lead investors have ideas about founder’s capabilities, and market potential, startups in the early stages of capital raising face uncertainty about their ultimate outcomes. Investors incur the most risk during the pre-seed and seed rounds and they have turned their attention to repositioning current portfolios rather than investing in new ventures given falling valuations. While big pharma is flush with cash, busy seeking bolt-on acquisitions and partnerships, emerging companies are seeking ways to extend their cash runways by tightening their budgets, shedding excess space, and shutting down drug research lines that haven’t shown promise.

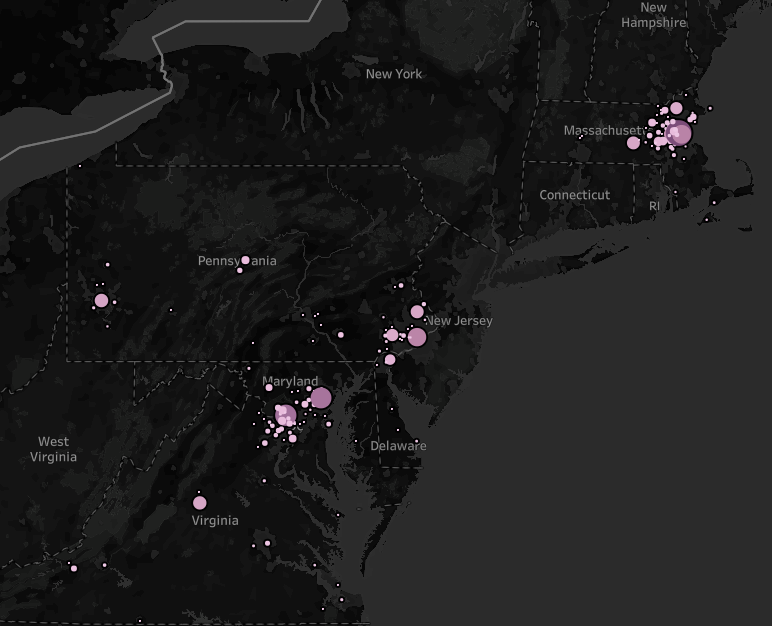

Early-stage companies are seeking alternative sources of capital such as the National Institute of Health Small Business Innovation Research (SBIR) program, that “[supports] early-stage companies seeking to commercialize innovative biomedical technologies.”7 Federal grant support to startups is a strong indicator of future growth and have an essential role in maintaining a strong life science ecosystem. Current funding has followed the macro trends, falling 38.98% quarter over quarter from 2022, lagging the most recent lows in 2018.8 The silver lining is that CY Q3 has historically seen the largest outflows of grant funding for seed stage companies via government programs. NIH has a mandate to maintain their efforts to supplement private sector capital to support federal R&D, create jobs, and strengthen supply chains, accelerated by Biden’s National Biotechnology and Biomanufacturing Initiative9. These funding channels have continued to flow into the well-known clusters of the I-270 Corridor, Philadelphia, and Boston.

NIH SBIR FUNDING 2018-2023 MATCHES CLUSTERS

Source for Map: NIH SBIR Funding, Scheer Partners. Note: Excludes NY, NJ.

While Scheer Partners remains bullish on the fact that science never stops, the slowdown of available capital has become extremely evident. We will see a lot of companies in need of lab space over the next year particularly for incubators or smaller spec suites10. It’s important to recognize that the associated real estate requirements take time - searches can range between three-to-six months to identify existing facilities. For startup and early-stage tenants in the market, it might be time to evaluate your cash runway and prioritize capital outflows, while planning your real estate footprint to prepare for the second half of the year.

1 Amortized cost.

2 Silicon Valley Bank. Q4, 10K. Loans.

3 Held-to-maturity (HTM) securities provide investors with a consistent stream of income; however, they are not ideal if an investor anticipates needing cash in the short-term (Investopedia).

4 Silicon Valley Bank. 2022 Form 10-K. SEC Filings.

5 Scheer Partners defines “Mid-Atlantic” as the major gateway markets in DE, DC, MD, NJ, NY, PA, VA. Scheer Partners currently has regional offices in Rockville, MD and Philadelphia, PA. 6 As of 3/28/23.

7 Small Business Innovation Research from NIH Seed Fund. Currently $1.2B. SBIR.NIH.COM.

8 As of 3/30/23.

9 Biden Administration Executive Order announced in September 2022 to invest more than $2B. White House Fact Sheet.

10 Spec-suites are pre-constructed lab space(s) that are move-in ready.

Images

Additional Info

Related Links : https://files.constantcontact.com/b9cbea97001/4e344a25-5572-4112-8277-c04a50313058.pdf

Powered By GrowthZone